Go woke. Go broke. Have the Fed bail you out.

As I watched the sudden collapse of the Silicon Valley Bank, I marveled once again at how a geezer’s administration run by tokens of diversity can wreck the economy by turning mundane functions — say, unloading transport ships — into extraordinary catastrophes, such as a supply chain backlog.

Train wrecks happen, sure, but it takes a special innate incompetence to have the EPA set fire to the toxic contents spilled over the tracks in East Palestine, Ohio, sending a black cloud into the air that was seen for miles around as it spread the danger over hundreds of square miles.

I am awestruck by the ineptitude of a Department of Transportation that spends billions of dollars not to build roads but to destroy them in the name of fighting racism.

The return of inflation after a 40-year hiatus tops the list of Biden’s calamities. Thus far the administration’s answer is to keep borrowing and spending as if there is no tomorrow in the fervent and erroneous belief that this will make it go away, when in fact all it does is fuel inflation.

No idea is too kooky for these Ivy League-educated idiots. The Los Angeles Times reported, “How white and affluent drivers are polluting the air breathed by L.A.’s people of color.”

The story said, “Angelenos who drive less tend to be exposed to more pollution.

“It may sound like a paradox, but it’s not. It’s a function of the racism that shaped this city and its suburbs, and continues to influence our daily lives — and a stark reminder of the need for climate solutions that benefit everyone.”

The people who live near freeways are poor and the LA Times presumes they all are people of color. Look for Biden and his Band of Bimbos to destroy freeways in Southern California in his second term and turn them into more camps for the homeless. This will continue until liberals decide that because most homeless people are white that homelessness is white privilege and start destroying the camps.

Behind every disaster, of course, is a token that Biden appointed to be the first fill-in-the-blank.

The smoke-’em-if-you-got-’em EPA is run by its first male black administrator. The first woman Treasury secretary is overseeing the return of inflation. The first Homeland Security secretary born in Cuba gave us the biggest border crisis in American history. The first Latino Health and Human Services secretary gave us a shortage of baby formula.

And of course, the man behind the supply chain problem, the airline crisis, and the destruction of highways is the first homosexual Cabinet member not named Ric Grenell.

The collapse of the Silicon Valley Bank is the shiniest example of failure. For 4 decades, SVB financed the mining of tech-industry gold. Biden demolished it in two years.

Reuters reported, “Based in Santa Clara, the lender was ranked as the 16th biggest in the U.S. at the end of last year, with about $209 billion in assets. Specifics of the tech-focused bank's abrupt collapse were a jumble, but the Fed's aggressive interest rate hikes in the last year, which had crimped financial conditions in the startup space in which it was a notable player, seemed front and center.

“As it tried to raise capital to offset fleeing deposits, the bank lost $1.8 billion on Treasury bonds whose values were torpedoed by the Fed rate hikes.”

Those rate hikes were to cure the inflation that the first woman Treasury secretary resurrected from the dead.

Without any sense of irony, White House Council of Economic Advisers chair Cecilia Rouse told Fox, “Our banking system is in a fundamentally different place than it was, you know, a decade ago. The reforms that were put in place back then really provide the kind of resilience that we’d like to see.”

Need I say she is the first black woman to serve in that office? Need I also point out that the collapse actually shows those alleged reforms failed?

California regulators shuttered SVB after they noticed depositors suddenly withdrew $42 billion from the bank on Thursday.

On Sunday, CNBC reported, “U.S. regulators on Sunday shut down New York-based Signature Bank in a bid to prevent the spreading banking crisis.”

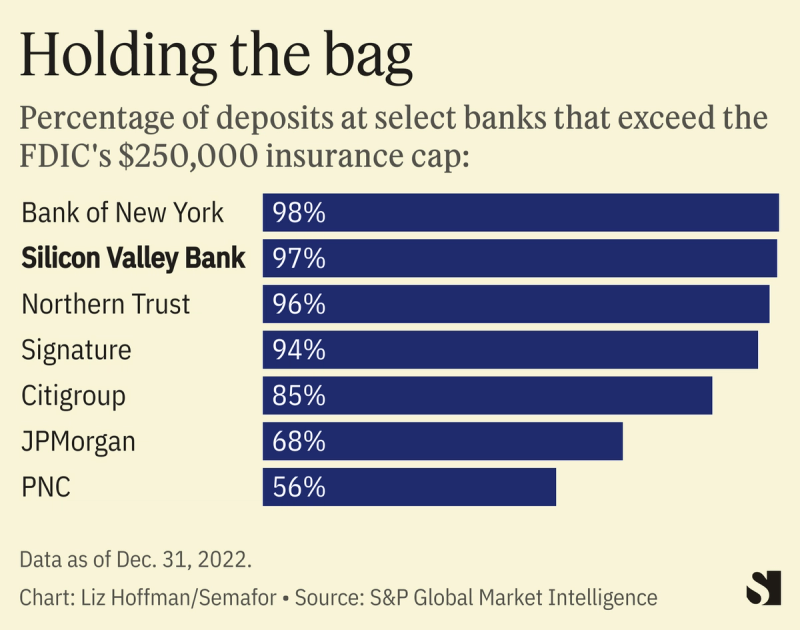

I believe it is too late to prevent the inevitable. Too many banks are holding onto too many deposits that are uninsured. 94% of Signature’s deposits were uninsured. The dirty little secret is FDIC insured deposits are small at big banks.

56% of PNC’s deposits are uninsured. 68% at JPMorgan. 85% at Citigroup. 98% at Bank of New York. Who will cover for them?

{kind=link}

Don’t think it can’t happen to them because it will. SVB was a winner until Biden came along.

Bill Biggerstaff and Robert Medearis founded SVB in 1983 as a conduit for venture capitalists to invest in Silicon Valley startups. The bank’s fortunes rose with the rise of companies founded in the Bay Area. Later it expanded into real estate and wineries. In retrospect, it was destined to succeed because the bank helped finance the economic colossus we call Silicon Valley. It is to the 21st century economy what Detroit and Pittsburgh were to the 20th century’s economy.

The money poured into SVB like it did to Studio 54 in the coke-craven 1970s and 1980s. Unlike that New York disco, the money was legal and not kept in garbage bags, but the amounts deposited were outside the FDIC’s coverage.

97% of its deposits were uninsured. As the big banks spin this as the fault of the FDIC, remember they seek insurance coverage of money they did not insure. SVB paid insurance premiums for only 3% of its deposits. That is all the money it is entitled to. These are the rules the banks wanted because if the banks wanted the coverage, they would have gotten Congress to cover them.

If you go uninsured and you wreck your car, you pay to fix it. The same should be true with bank deposits. I get that the feds limit their insurance to the first $250,000 of each depositor’s money. But why isn’t there a secondary insurer? Why don’t the Aflac duck and the Geico gecko get together and provide insurance for deposits above $250,000? They could hire Flo to pitch their insurance.

We know why not. The rich already have insurance on their uninsured balances. It is called Congress. The rich know if they apply enough pressure from a foolish public, the rich always can get another bailout.

However, the word bailout freaks out the public. Enter the Federal Reserve — you know, the people whose rate hikes caused SVB to fold. Taxpayers won’t cover the uninsured deposits. The Federal Reserve will.

The Fed said, “To support American businesses and households, the Federal Reserve Board on Sunday announced it will make available additional funding to eligible depository institutions to help assure banks have the ability to meet the needs of all their depositors. This action will bolster the capacity of the banking system to safeguard deposits and ensure the ongoing provision of money and credit to the economy.

“The Federal Reserve is prepared to address any liquidity pressures that may arise.

“The additional funding will be made available through the creation of a new Bank Term Funding Program, offering loans of up to one year in length to banks, savings associations, credit unions, and other eligible depository institutions pledging U.S. Treasuries, agency debt and mortgage-backed securities, and other qualifying assets as collateral. These assets will be valued at par. The BTFP will be an additional source of liquidity against high-quality securities, eliminating an institution's need to quickly sell those securities in times of stress.

“With approval of the Treasury Secretary, the Department of the Treasury will make available up to $25 billion from the Exchange Stabilization Fund as a backstop for the BTFP. The Federal Reserve does not anticipate that it will be necessary to draw on these backstop funds.”

So magically — without authorization or funding from Congress — the Fed on a Sunday afternoon created a $25 billion spending program because no one in the press or Congress will protest. It just does what it wants when it wants as it continues to prop up an economy gutted by cheap Chinese imports. That this program will only encourage more folly by bankers goes without saying.

Who came up with this crazy unconstitutional idea? Mark Cuban, who just happens to have $10 million or so on deposit at SVB.

He tweeted, “The Fed should IMMEDIATELY buy all the securities/debt the bank owns at near par, which should be enough to cover most deposits. Any losses paid for in equity and new debt from the new bank or whoever buys it. The Fed knew this was a risk. They should own it.

“If the Fed doesn’t own it, trust in the banking system becomes an issue. There are a ton of banks with more than 50% uninsured deposits.”

Trust in the banking system should be the issue because banking is almost as untrustworthy as the news media. Banks collapsed the economy in 2008 with sub-prime loans that wrecked local housing markets by giving mortgages to people with no means (or intention) to pay the money back. Prices rose as they bought — and crashed when they defaulted.

If you want trust, earn it. This action does not earn trust because it smells like panic and favoritism.

Glenn Reynolds at Instapundit wrote, “In the comments, people point out that SVB is a techbro bank, and they’re Dem donors, while Signature has Barney Frank on its board. You people are so cynical.”

The Fed creating a new program merely kicked the can down the road. The bigger banks also have more money deposited than is insured by the FDIC. The reaction to SVB’s crash is a harbinger of what will happen when bigger banks go under.

However, Kane at Citizen Free Press said, “We hate bailouts for bondholders and shareholders. No one is getting bailed out. The CEO is still fired. Bondholders and stockholders lose everything.

“But this is about protecting depositors and business payrolls. If you are a small business with a $2 million monthly payroll, you would have to keep your money in 10 different banks, and coordinate your weekly payroll with 10 banks, in order to stay under the $250,000 FDIC limit.”

So raise the limit. Make it $10 million and extend the premiums to cover the additional liability for the FDIC. It is not as if the government isn’t covering these deposits anyway. Also, limit how much uninsured deposits banks can have. If 97% uninsured was too big for SVB, what makes 98% at Bank of New York OK?

Congress could raise the required limit today and the FDIC could start collecting the premiums tomorrow.

But that won’t happen because for some reason, Washington will limit how large your toilet tank is but won’t crack down on the banking industry. It is as if the banks own the government.

Now that President Trump is out of the way, it is business as usual in DC. That’s the scary part because the people in DC no longer are the best and the brightest (who, by the way, got us into Vietnam) but the odd and unusual.

As were the people running this bank.

Zero Hedge pointed out that as it died, SVB still pushed DEI — diversity, equity and inclusion. Zero Hedge said, “You see, SVB believes ‘inclusion ignites innovation,’ although I guess liquidity wasn't part of the ethos.”

Go woke. Go broke. Have the Fed bail you out.

This situation is the son of the $700 billion bailout from 2008-2009.

Pundits say the bankers learned nothing from that debacle but they learned plenty — mainly that they can ignore the rules because Uncle Sam will always bail them out.

This time, the bailout did not include taxpayer money. Instead, the Fed will print up another $25 billion to feed the fires of inflation. Next time, taxpayer money will be needed because all those banks that are Too Big To Fail are not big enough to cover Biden’s many, many calamities.

Giving billions of dollars to people who promote and support things like DEI, ESG, LGBQT, etc is not productive investment. "The whole of government" (as they say) is now laser-focused on keeping itself in power. The Silicon Bank failure is (I believe) a federally produced event to distract from what Pence-Pelosi-Schumer-McConnell accomplished on January 6th 2021: The Parliamentary Motive Behind the J6 Fedsurrection https://theconservativetreehouse.com/blog/2023/03/12/the-parliamentary-motive-behind-the-j6-fedsurrection/

I can certainly attest to your comments about PNC Bank. When I went to renew my CD's back in February, I saw that my two IRA's had actually LOST money. The banker I spoke to said that he could renew my IRA's now paying 4%. I said "You have 100K of my money and you are deducting fees ?" I could not contain my anger. I told this idiot to close my accounts and I will never EVER do business with PNC again.

To the fools who voted for a senile jackass like Joe Biden, not that were many that really did, yolu got what you wanted and we will all pay the price. If you haven't prayed before, now is a good time as any to start.